| Star | Watch | Fork |

| Home |

|---|

| User Guide |

| Examples |

| About |

Robust Portfolio

In this example, the portfolio construction problem discussed in the previous sections is solved by a robust optimization approach introduced in the paper Bertsimas and Sim (2004). The robust model is presented below.

\[\begin{align} \max~&\min\limits_{\pmb{z}\in\mathcal{Z}} \sum\limits_{i=1}^n\left(p_i + \delta_iz_i \right)x_i \\ \text{s.t.}~&\sum\limits_{i=1}^nx_i = 1 \\ &x_i \geq 0, ~\forall i = 1, 2, ..., n, \end{align}\]where the affine term \(p_i + \delta_iz_i\) represents the random stock return, and the random variable is between \([-1, 1]\), so the stock return has an arbitrary distribution in the interval \([p_i - \delta_i, p_i + \delta_i]\). The uncertainty set \(\mathcal{Z}\) is given below,

\[\begin{align} \mathcal{Z} = \left\{\pmb{z}: \|\pmb{z}\|_{\infty} \leq 1, \|\pmb{z}\|_1 \leq \Gamma\right\}, \end{align}\]where \(\Gamma\) is the budget of uncertainty parameter. Values of the budget of uncertainty and other parameters are presented as follows.

\[\begin{align} & \Gamma = 5 &\\ & p_i = 1.15 + i\frac{0.05}{150}, &\forall i = 1, 2, ..., n \\ & \delta_i = \frac{0.05}{450}\sqrt{2in(n+1)}, &\forall i = 1, 2, ..., n. \end{align}\]The robust optimization model can be implemented by the following Python code.

from rsome import ro

from rsome import grb_solver as grb

import rsome as rso

import numpy as np

n = 150 # number of stocks

i = np.arange(1, n+1) # indices of stocks

p = 1.15 + i*0.05/150 # mean returns

delta = 0.05/450 * (2*i*n*(n+1))**0.5 # deviations of returns

Gamma = 5 # budget of uncertainty

model = ro.Model()

x = model.dvar(n) # fractions of investment

z = model.rvar(n) # random variables

model.maxmin((p + delta*z) @ x, # the max-min objective

rso.norm(z, np.infty) <=1, # uncertainty set constraints

rso.norm(z, 1) <= Gamma) # uncertainty set constraints

model.st(sum(x) == 1) # summation of x is one

model.st(x >= 0) # x is non-negative

model.solve(grb) # solve the model by Gurobi

Being solved by Gurobi...

Solution status: 2

Running time: 0.0038s

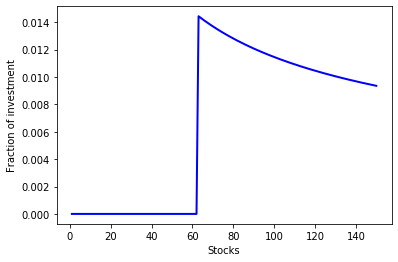

The optimal investment decision can be visualized by the diagram below.

import matplotlib.pyplot as plt

obj_val = model.get() # the optimal objective value

x_sol = x.get() # the optimal investment decision

plt.plot(range(1, n+1), x_sol, linewidth=2, color='b')

plt.xlabel('Stocks')

plt.ylabel('Fraction of investment')

plt.show()

print('Objective value: {0:0.4f}'.format(obj_val))

Objective value: 1.1709

Reference

Bertsimas, Dimitris, Melvyn Sim. 2004. The price of robustness Operations Research 52(1) 35–53.